Insurance is a critical part of modern life, providing financial protection against unexpected events. Whether it’s for your car, home, health, or business, insurance offers a way to manage risks and protect your assets. However, many people may not fully understand how insurance works or how insurance companies operate. In this article, we will explore the basics of insurance, how it works, and provide key information about insurance companies to help you make informed decisions.

What is Insurance?

At its core, insurance is a contract between an individual or entity (the policyholder) and an insurance company. In exchange for regular payments called premiums, the insurance company agrees to cover certain losses or damages as specified in the policy. Insurance helps to mitigate financial risks associated with accidents, illnesses, natural disasters, and other unforeseen events.

Key Concepts in Insurance

- Premiums: The amount the policyholder pays regularly (monthly, quarterly, or annually) to keep the insurance coverage active. Premiums vary based on factors such as the type of insurance, the policyholder’s risk profile, and the coverage amount.

- Policy: The insurance contract that outlines the terms and conditions of coverage, including what is and isn’t covered, the coverage limits, and any exclusions.

- Deductible: The amount the policyholder must pay out of pocket before the insurance company starts covering a claim. Higher deductibles usually result in lower premiums.

- Claim: A formal request made by the policyholder to the insurance company for coverage or compensation for a covered loss or event.

- Coverage: The specific events or risks that the insurance policy will protect against. For example, a car insurance policy may cover accidents, theft, and vandalism.

- Exclusions: Specific circumstances or events that are not covered by the policy. It’s important to understand these exclusions before purchasing insurance.

Types of Insurance

There are various types of insurance available, each designed to cover different aspects of life. Here are some of the most common types of insurance:

1. Health Insurance

Health insurance helps cover medical expenses, including doctor visits, hospital stays, surgeries, prescription medications, and preventive care. In most cases, policyholders pay a monthly premium, and the insurance company covers a portion of their medical costs.

There are different types of health insurance plans, including:

- HMO (Health Maintenance Organization): Requires policyholders to choose a primary care physician and get referrals for specialist visits.

- PPO (Preferred Provider Organization): Offers more flexibility in choosing healthcare providers and does not require referrals for specialists.

- EPO (Exclusive Provider Organization): Limits coverage to doctors and hospitals within the plan’s network, except in emergencies.

2. Auto Insurance

Auto insurance provides financial protection against damage to your vehicle, as well as liability for injuries or damage caused by an accident. Coverage typically includes:

- Liability: Covers damage or injury to others if you’re at fault in an accident.

- Collision: Covers repairs to your own vehicle in the event of an accident.

- Comprehensive: Covers non-accident-related damages, such as theft, vandalism, or weather-related damage.

3. Homeowners Insurance

Homeowners insurance covers your home and personal property in the event of damage or loss caused by perils like fire, theft, or natural disasters. It also provides liability coverage if someone is injured on your property. Coverage may include:

- Dwelling Coverage: Protects the physical structure of your home.

- Personal Property Coverage: Covers the contents of your home, such as furniture, electronics, and clothing.

- Liability Coverage: Provides financial protection if someone is injured on your property or if you’re found liable for property damage.

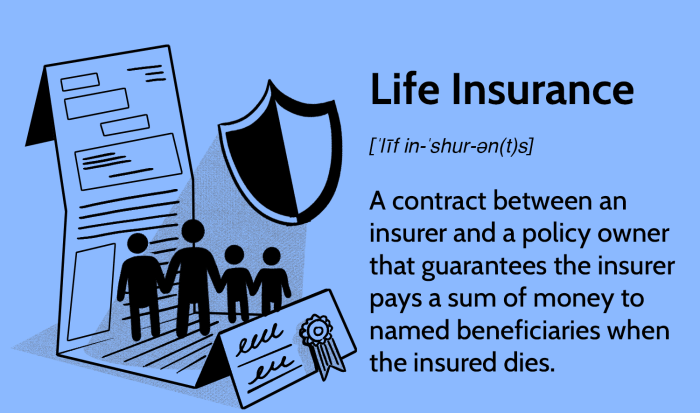

4. Life Insurance

Life insurance provides a financial payout to beneficiaries upon the policyholder’s death. The two primary types of life insurance are:

- Term Life Insurance: Provides coverage for a specific period, such as 10, 20, or 30 years. If the policyholder dies during the term, the beneficiaries receive the death benefit.

- Whole Life Insurance: Provides coverage for the policyholder’s entire life and includes an investment component, allowing the policyholder to build cash value over time.

5. Business Insurance

Business insurance helps protect businesses from financial losses due to risks such as property damage, lawsuits, and employee injuries. Common types of business insurance include:

- General Liability Insurance: Covers legal costs if the business is sued for causing injury or property damage.

- Property Insurance: Covers damage to the business’s physical assets, such as buildings and equipment.

- Workers’ Compensation Insurance: Covers medical expenses and lost wages for employees injured on the job.

How Does Insurance Work?

The basic principle behind insurance is risk pooling. By spreading the financial risk across a large group of policyholders, insurance companies can afford to cover the costs of the relatively few who experience significant losses. This is how it works:

- Risk Assessment: Insurance companies assess the risk of insuring individuals or businesses by evaluating factors such as age, health, occupation, and driving history. This assessment helps determine the likelihood of a claim being made.

- Premium Calculation: Based on the risk assessment, the insurance company calculates the premium—the amount the policyholder must pay to maintain coverage. Higher-risk individuals or entities typically pay higher premiums.

- Underwriting: The underwriting process involves evaluating and deciding whether to approve the insurance application. If the insurance company accepts the risk, the policy is issued to the policyholder.

- Claims Process: When an insured event occurs, the policyholder files a claim with the insurance company. The company will investigate the claim to verify that the loss is covered under the policy. Once verified, the company will either repair or replace the damaged property or provide a financial payout.

- Payouts: Insurance payouts are either made directly to the policyholder or to a third party, such as a medical provider or auto repair shop. The amount of the payout is determined by the terms of the policy, including any applicable deductibles.

Insurance Companies: How They Operate

Insurance companies play a crucial role in the insurance process, acting as intermediaries between policyholders and the financial resources that cover their claims. Here’s an overview of how insurance companies operate:

1. Risk Management

Insurance companies are in the business of managing risk. They assess the likelihood of an event happening (such as a car accident or house fire) and then price their policies accordingly. By pooling risk across many policyholders, insurance companies can protect themselves against large, unpredictable losses.

2. Underwriting

Underwriting is the process by which insurance companies evaluate the risk associated with insuring a particular individual or entity. Underwriters review applications, assess risk factors, and decide whether to approve coverage. They also set premiums and determine the terms of the policy. The goal of underwriting is to ensure that the company is not taking on too much risk while still offering competitive prices.

3. Claims Processing

When policyholders experience a covered loss, they file a claim with the insurance company. The insurer will review the claim, verify coverage, and determine the appropriate payout. This process can vary in complexity depending on the type of insurance and the nature of the claim. For example, a simple auto repair claim may be settled quickly, while a complex business interruption claim may require extensive investigation and negotiation.

4. Profitability

Insurance companies make money in two primary ways:

- Premiums: The company collects premiums from policyholders and uses that money to pay claims. The company keeps any surplus as profit.

- Investments: Insurance companies invest the premiums they collect in a variety of financial instruments, such as bonds, stocks, and real estate. These investments generate additional income, which can help offset the cost of claims.

5. Regulation

Insurance companies are heavily regulated by both federal and state governments. Regulations are in place to ensure that companies remain financially solvent, treat policyholders fairly, and adhere to legal standards. In the U.S., insurance is primarily regulated at the state level, with each state having its own insurance department that oversees companies operating within its borders.

6. Reinsurance

Insurance companies sometimes purchase insurance themselves, a process known as reinsurance. Reinsurance allows companies to spread the risk of large claims across multiple insurers. For example, if an insurance company covers a high-value property, it may purchase reinsurance to reduce its exposure in case of a major loss. This helps insurance companies maintain financial stability and continue offering coverage even after significant claims.

Choosing the Right Insurance Company

When selecting an insurance company, it’s essential to consider several factors to ensure you are getting the best coverage for your needs:

- Financial Stability: Choose an insurance company with a strong financial rating from independent rating agencies such as A.M. Best or Moody’s. This ensures the company has the resources to pay claims.

- Reputation: Research customer reviews and ratings to understand how the company handles claims and customer service.

- Coverage Options: Ensure the company offers the specific types of coverage you need, whether it’s health, auto, home, or business insurance.

- Premiums and Deductibles: Compare premiums and deductibles across different companies to find a policy that fits your budget without sacrificing coverage.

Conclusion

Insurance is a vital tool for managing risks and protecting your financial future. By understanding how insurance works and how insurance companies operate, you can make informed decisions when choosing the right coverage